BDCs Look Cheap. The Question Is Why?

This is not a buying spree. It is a sorting phase.

A Note on Open Access

Once again, I am keeping this article outside of the paywall because I believe the concept of “Income Honesty” is too fundamental to be restricted. Whether you are a long-time subscriber or just starting to look at your first BDC, you deserve to know if the income you are counting on is actually being earned.

I spent some time working through the latest Wells Fargo BDC scorecard1 and it is worth slowing down on what is actually being said. On the surface, the sector looks attractive. Discounts are wider than usual and valuations screen as cheap. That tends to pull people in. But the report is not really making a valuation call. It is pointing to something happening underneath the surface that matters more.

The Earnings Engine Is Starting to Tighten

The issue is the earnings engine. BDCs make money on the spread between what they earn on loans and what it costs them to fund those loans. That spread is called net interest margin. In simple terms, if a BDC lends at 11% and its cost of capital is 7%, the margin is 4%. That 4% is what ultimately supports the dividend and protects the balance sheet. Right now, that margin is getting squeezed. Loan yields are starting to drift lower as the cycle matures, but funding costs have not fully adjusted. When that happens, earnings tighten.

At the same time, credit is no longer as clean as it was over the past few years. There is a steady increase in underperforming loans across the sector. Nothing that looks like a crisis, but enough to matter. The more important point is that there is not much excess cushion left in the system. If credit continues to soften, there is less room to absorb it without it flowing through to income or asset values. That is where you start to see pressure on dividends and gradual drift in NAV, which is simply the underlying value of the portfolio.

Where the Pressure Actually Begins

The line that stayed with me from the report is the idea that this is an equity problem. That sounds abstract, but it is actually quite simple. Most of the companies that BDCs lend to are backed by private equity. If those businesses start to struggle, whether because growth slows or refinancing becomes harder, the pressure shows up first in the equity layer. Over time, that pressure moves up the capital structure and into the loans themselves. That is how lenders start to feel it. This is why credit cycles rarely begin with the lender. They work their way up.

So this is not just a case of the market being overly pessimistic and offering bargains. Some of the discounts are there for a reason. The job now is to separate temporary dislocation from real deterioration. That is where selectivity matters.

Selectivity Matters More Than Yield

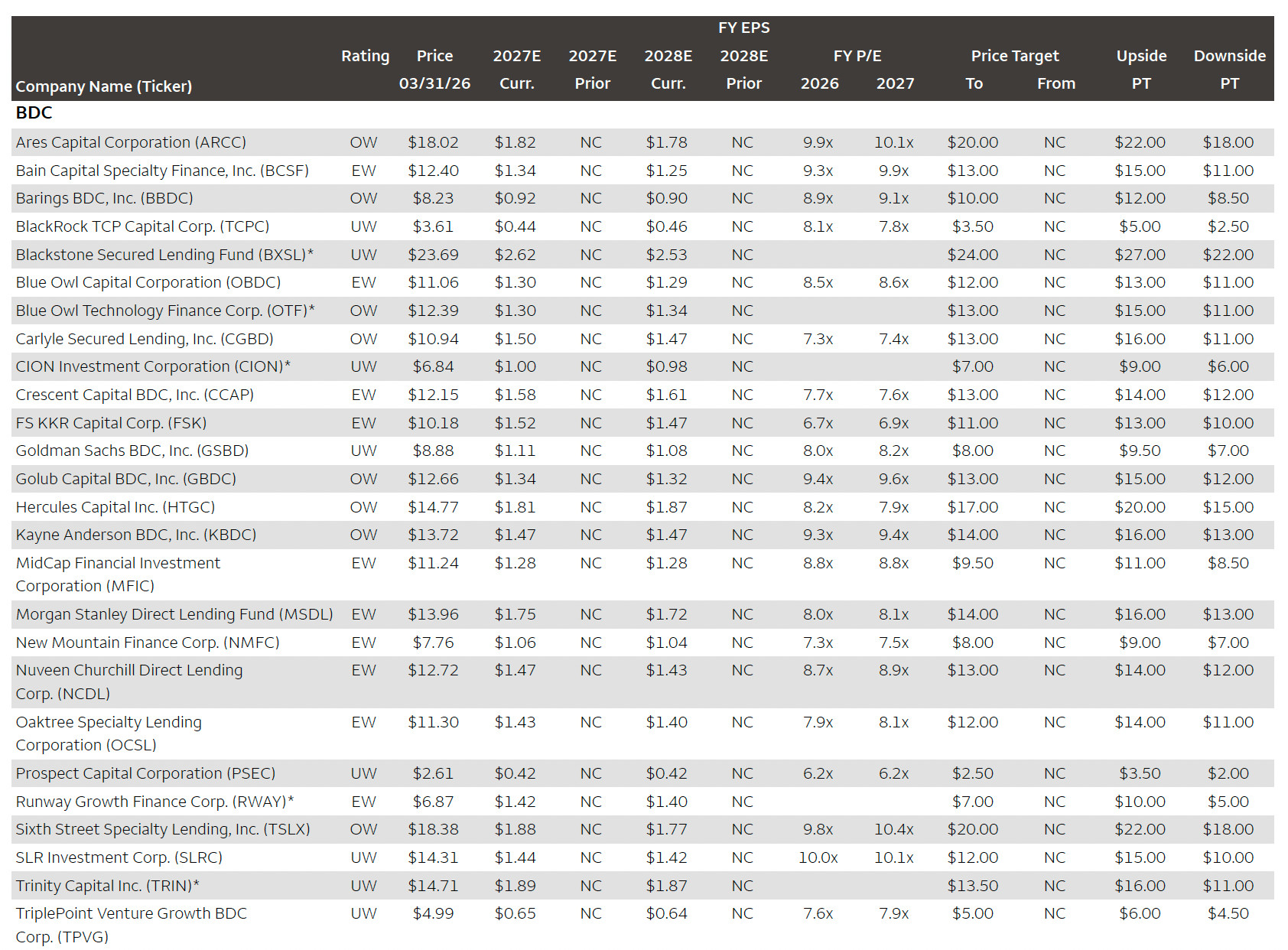

There are still a number of names that appear better positioned to come through this period. Sixth Street Specialty Lending (TSLX) stands out for its underwriting discipline and history of protecting capital rather than stretching for yield. Ares Capital Corporation (ARCC) brings scale and diversification, which tend to matter more as conditions tighten. Blackstone Secured Lending Fund (BXSL) has a relatively clean portfolio and strong sponsor backing. Even Barings BDC (BBDC) starts to look more interesting where the valuation reflects a more realistic view of the risks.

This is not about making recommendations and it is not about calling a bottom. It is about understanding what you own. The common thread across the stronger names is not yield. It is that they do not need everything to go right in order to maintain their income. That is a very different starting point.

A Sorting Phase

On the other side, there are parts of the market where yields are rising because prices are falling and earnings are coming under pressure. That can look attractive on a screen, but it is often where problems build. If income is not being fully earned, or if credit quality is slipping, the yield can end up being a distraction rather than an advantage.

This feels like a sorting phase rather than a broad opportunity. Some income streams will hold up and continue to compound over time. Others will look fine for a while and then gradually erode. From the outside, they can appear very similar. The difference only shows up if you look at what is happening inside the portfolio.

That is where the work is right now.

Predictable Yield Engine is for investors who want structure, not stock tips.

Paid subscribers get access to the full PYE Playbook: portfolio architecture, capital allocation rules, reinvestment discipline, and how I actually size and adjust risk through market cycles. If you’re building an income portfolio meant to compound over time, that’s what the subscription unlocks. Subscribe here to get full access.

Disclaimer

The analysis and commentary shared here reflect my own research and investment approach. This content is provided for informational and educational purposes only and should not be considered financial advice, a recommendation to buy or sell any security, or an endorsement of any particular strategy. Nothing here is tailored to the investment needs or circumstances of any individual. Charts, graphs, or figures are illustrative only and should not be relied upon as the basis for investment decisions. Please consult a qualified financial advisor before making investment choices that may affect your personal financial situation.

1Q:26 BDC Scorecard “It’s An Equity Problem. Wells Fargo April, 2026

Thank you for posting the spread sheet. I like the upside /downside PPS valuations. Conservative numbers . Have a great weekend!