When the Average Economy Stops Being Useful

Beyond the Blended Numbers: Why Market Averages Are Hiding the Risks & Opportunities in a Fractured Economy

I always enjoy David Kelly’s writing because he has one of the better panoramic views on markets. Kelly is Chief Global Strategist at J.P. Morgan Asset Management, and his work is useful because he does not look at markets through one narrow lens. He connects the economy, consumers, politics, corporate earnings, valuations and investor behavior into one broader picture. His latest piece, Investing in a Divergent Economy, from his regular blog is worth reading for that reason.

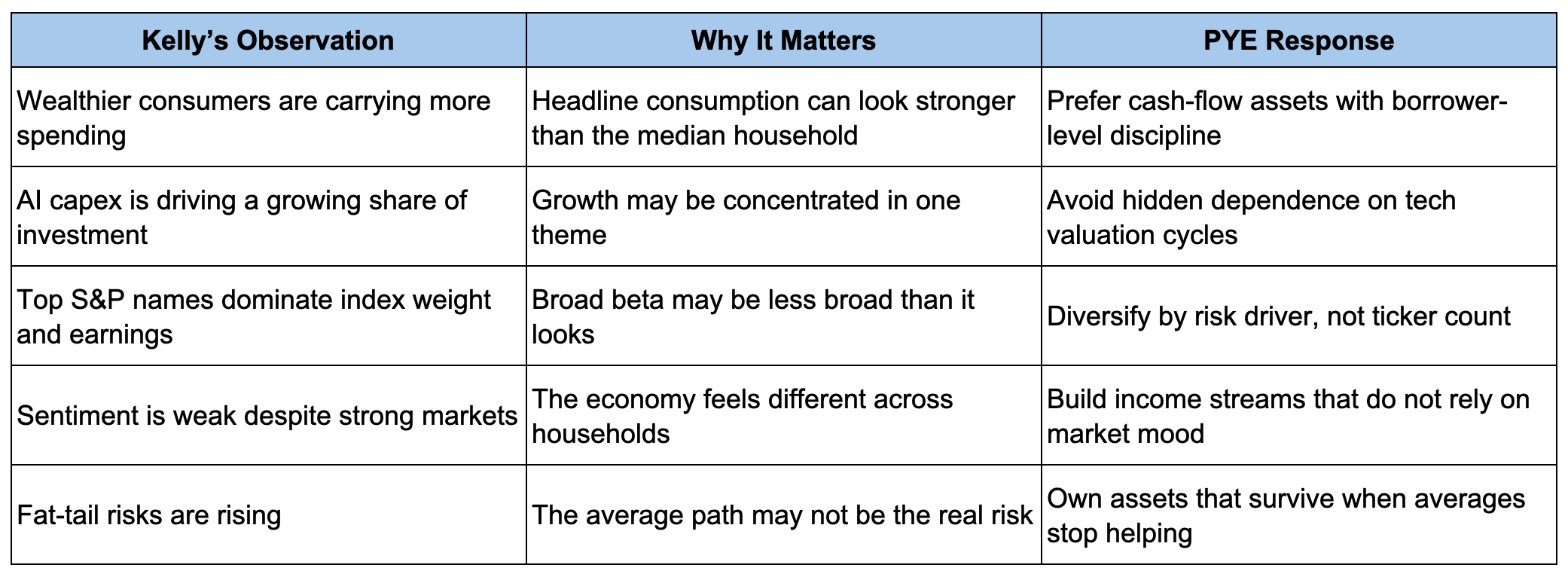

The central point is simple but important: the economy does not look broken at the headline level, but the averages are hiding a lot of stress underneath. Growth is still positive. Employment is still holding up. Markets have been strong. Wealthier consumers are still spending. AI investment continues to pull huge amounts of capital into the system. On the surface, the average path still looks reasonably benign. But the average is doing a lot of work.

Kelly’s point is that the economy underneath that average is becoming more divided. Richer households are driving a growing share of spending. Technology, and especially AI-related capital spending, is carrying a larger share of growth. Asset prices have become a bigger part of economic confidence. Meanwhile, many ordinary consumers are dealing with wage pressure, inflation fatigue and a much less forgiving cost structure. That matters because averages can hide risk. Averages tell us what the economy looks like when everything is blended together. They do not tell us who is carrying the load, who is weakening, and where the next break may occur. For investors, that distinction matters.

The Headline Can Be Right And Still Mislead You

One of the mistakes investors make is assuming that a decent macro backdrop automatically means risk is low. It does not. A divergent economy can keep producing acceptable headline numbers even while risk is concentrating underneath. GDP can look fine because wealthy households are still spending. Earnings can look fine because a narrow group of companies is doing the heavy lifting. The stock market can look fine because a handful of mega-cap technology names are carrying the index.

None of that means the underlying system is broadly healthy. It means the average is being pulled higher by a narrower set of drivers. That is not automatically bearish. I am not making a recession call here. I am not saying AI is fake. I am not saying wealthy consumers are about to stop spending. I am saying the investment problem changes when the economy becomes this dependent on fewer supports. The key question becomes less about predicting the next macro number and more about understanding what you actually own.

The real-world data from the credit markets has already validated this divergence. Historical credit datasets establish that the long-term historical baseline for corporate loan failures sits near ~3%. Projections from Moody’s Analytics anticipated that the actual U.S. leveraged loan default rate would face severe upward trajectory pressure, targeting a peak near 7.5% to 7.9%.1 Realized performance data verified that these default levels fully materialized, matching the forecasted range and tracking at more than twice the long-term historical average. When headline economic growth masks systemic credit failures of this magnitude, relying on broad economic averages becomes hazardous.