Standard Life: From Hidden 8% Yield to Validated Retirement Cash Machine

May 2026 Update: The Thesis Has Been Validated

When I first wrote about Phoenix Group in December 2025, the company was still largely viewed as a complicated legacy UK life insurer. That was the opportunity. The public market was focused on accounting noise, closed-book complexity, and the usual suspicion around insurance balance sheets. The underlying business looked very different.

Phoenix was not a general insurer. It was a retirement, pensions, and annuity platform with long-duration liabilities, predictable cash generation, spread income, and a growing fee-based savings business. In other words, it was beginning to resemble the kind of permanent-capital engine that private credit firms have spent the last decade trying to build around annuity balance sheets.

Since then, the story has moved on. Phoenix has now officially completed its rebranding as Standard Life plc, trading under the new London Stock Exchange ticker SDLF.L. The latest FY25 results and the blockbuster proposed Aegon UK acquisition make the original thesis stronger. The business is larger, cleaner, more strategically focused, and more obviously positioned as one of the core platforms in the UK retirement savings and income market.

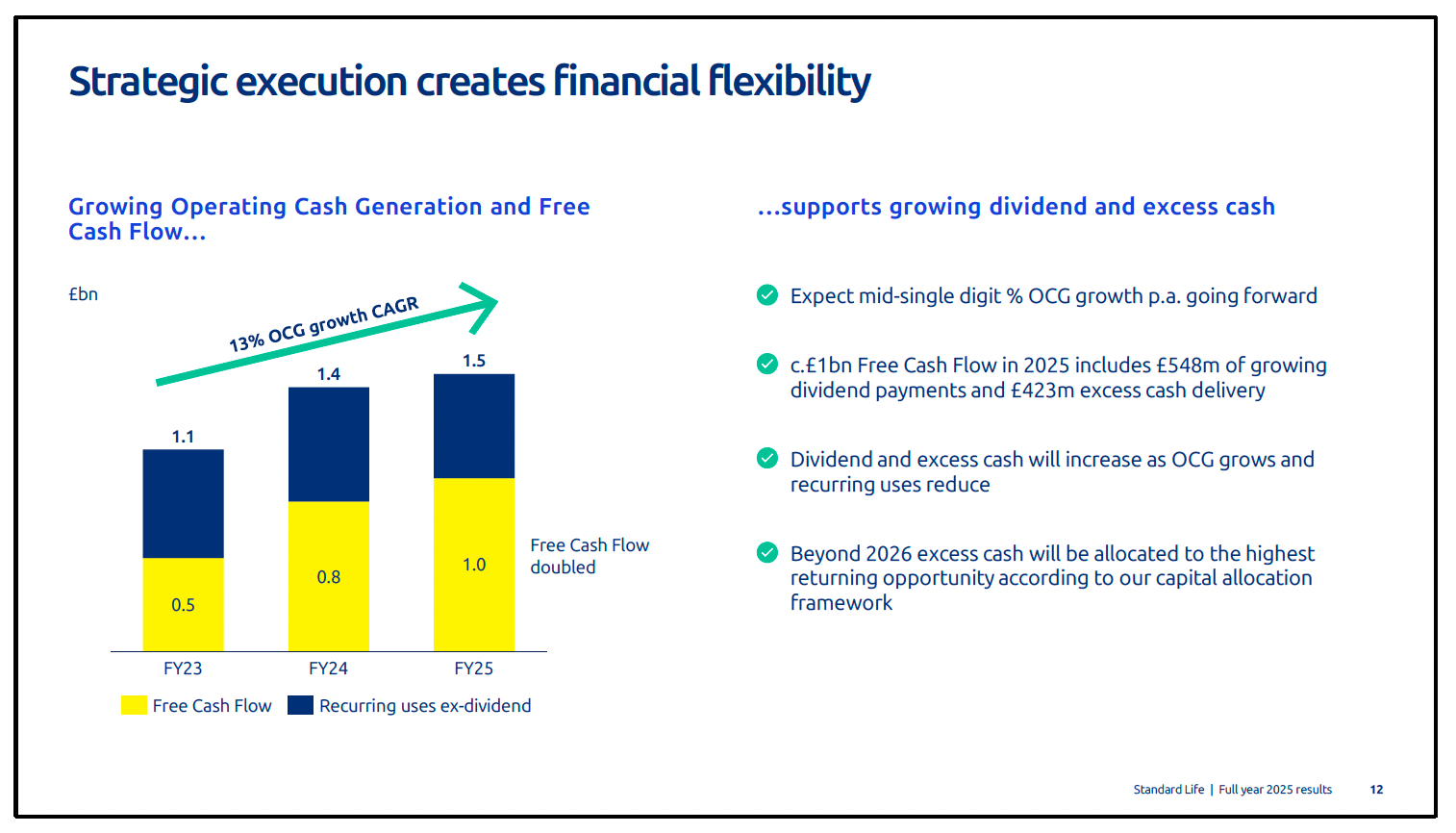

The price has moved too, and that matters. At around 794p, using the newly announced FY25 dividend of 55.40p, the yield is now roughly 7%, rather than the 8% level that made the original setup so compelling. The updated view is therefore more nuanced. The thesis has been completely validated, but the entry point is less generous.