MONY Group: A Case Study in Operational Compounding

Analyzing the 7.4% yield and the structural mechanics for US investors

Background

Before we dive into the architecture, we must define the opportunity. MONY Group PLC (formerly Moneysupermarket.com Group) is a cornerstone of the UK’s digital economy. Listed on the London Stock Exchange (LSE: MONY.L) and a constituent of the FTSE 250, the company operates the UK’s leading price comparison websites.

Founded in 1993, the business revolutionized how British households manage their finances. Today, it owns a portfolio of dominant brands: Moneysupermarket (insurance and loans), MoneySavingExpert (the UK’s most trusted financial advice consumer site), and Quidco (cashback). Essentially, MONY is a technology-led middleman; it earns a commission every time a user “switches” their car insurance, energy provider, or credit card through their platform. For a PYE investor, this is a play on the structural necessity of household thrift.

The core of the Predictable Yield Engine (PYE) is built upon a single, non-negotiable floor: we require an 8% cash yield from our primary income assets. This threshold serves as a structural filter, ensuring that our Core Anchors, the BDCs and CEFs that form the PYE Spine, generate enough natural velocity to sustain the portfolio without requiring the liquidation of principal.

MONY does not clear this floor. At a current price of 170.71p, its 2025 total dividend of 12.63p offers a yield of 7.4%. In a rigid framework, this is an automatic “pass.” However, much like our previous assessment of STEW, MONY presents a specific set of compounding mechanics that make it a compelling Satellite position. It is not an income engine, but it is “growth that pays rent.”

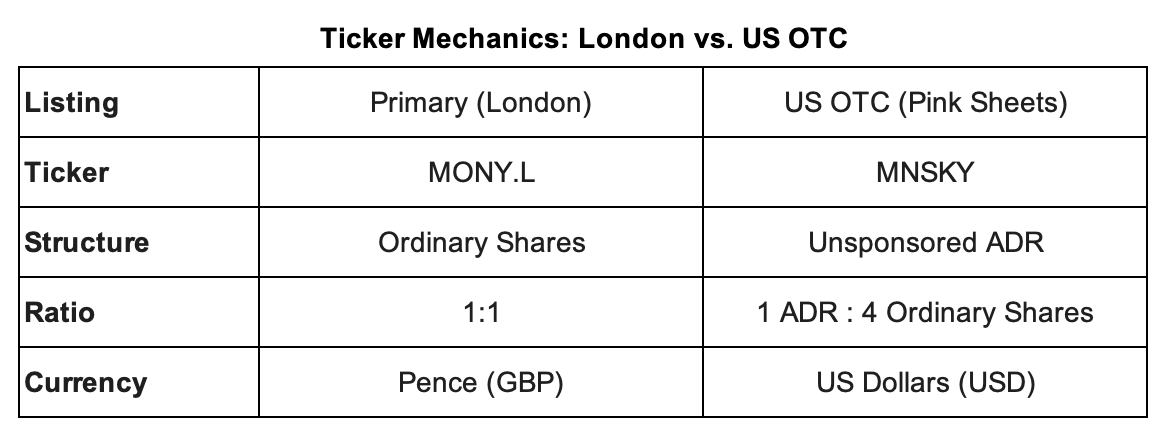

MONY trades in both the UK and via an OTC lising in the US. Details of these listings is included in the table, below.

I. Architectural Placement: The Dividend Growth Sleeve

In our established architecture, MONY does not fit the profile of a Core Anchor. It lacks the asset-backed downside protection of a Tanker or the discount-to-NAV appeal of an Extractor. While one might be tempted to label it as “Ballast,” MONY’s underlying revenue is too cyclical for that designation, evidenced by the 13% drop in Cashback and 10% drop in Travel revenues this year.

Instead, MONY occupies a seat in the Dividend Growth Sleeve. It sits outside the PYE Spine, at the boundary between accumulation and reliance. It earns its place not by clearing the 8% yield hurdle, but through its contribution to the system’s total durability. It provides a bridge of high-quality, covered cash flow that buffers the portfolio against the higher volatility of pure growth assets.

II. The 7.4% Yield: A Conversation on Quality

We must address the yield gap directly. A 7.4% yield is mathematically inferior to 8%. I am not going to pretend otherwise. What I am going to explain is why the quality of coverage, balance sheet structure, and compounding mechanics make this 7.4% more interesting than many assets that technically clear the threshold.

The dividend is covered 1.4x by Adjusted Basic Earnings Per Share (EPS) of 17.9p. While credit vehicles typically distribute 90–100% of earnings, MONY retains approximately 30% to reinvest in its technology platform and “rebuild dividend cover”.

Furthermore, MONY operates from a position of exceptional balance sheet strength:

Net Cash: The group ended 2025 with £4.1 million in net cash, a rare attribute for a high-yield seeker.

Zero Structural Debt: Their £125m Revolving Credit Facility (RCF) was repaid in full shortly after the reporting period.

While a 7.4% covered yield is the headline, the "Predictable Yield" thesis relies on the mechanics of the engine itself. Below, we move from the surface numbers to the proprietary PYE analysis: the arithmetic of synthetic yield, the AI-driven catalysts for margin expansion, and the specific structural mechanics that allow US investors to capture this as a "Qualified" distribution.